Introduction

GST registration under Rule 14A is a fast‑track option for small taxpayers who want a simpler, digital‑only way to get GST registration. Introduced through the CGST (Fourth Amendment) Rules, 2025, this scheme lets eligible businesses get GST registration approval within about three working days, without long‑drawn manual checks or physical verification.

If your monthly output tax liability on supplies to registered persons is not high and you use Aadhaar-based authentication, you can choose this fast-track option instead of the normal registration route. This article explains the conditions, step-by-step process, benefits, and common mistakes so you can decide whether this route suits your business.

What is GST Registration Under Rule 14A?

Rule 14A of the CGST Rules, 2017, creates a special electronic registration channel for small, low‑risk taxpayers. It doesn’t create a new tax system; it just alters the application process and speeds up GSTIN issuance.

Key points about Rule 14A GST registration:

- Optional: You can still use the normal GST registration process if you do not meet Rule 14A conditions.

- Time‑bound: Registration under Rule 14A must be granted within three working days from the date of submitting Form GST REG‑01, if all conditions are met.

- Fully digital: There is no physical verification; Aadhaar authentication and system‑based risk checks replace manual scrutiny.

In simple terms, this is a “fast lane” for small businesses that sell mainly to other registered persons and have low monthly tax liability.

GST Registration Under Rule 14A Conditions

To qualify for GST registration under rule 14a, you must meet specific conditions laid down in the CGST Rules. These conditions are meant to keep the scheme for genuine, low‑risk taxpayers.

Main eligibility criteria

- Monthly output tax limit: Your total output tax liability on supplies to registered persons (B2B) must not exceed ₹2.5 lakh per month. This includes CGST, SGST/UTGST, IGST, and Compensation Cess.

- No large B2B exposure: The limit is based on tax payable, not on overall turnover. If your B2B tax grows above ₹2.5 lakh in any one month, you should exit Rule 14A and move to normal registration.

- One GSTIN per State/UT under same PAN: You cannot hold more than one registration under the same PAN in a State or Union Territory under Rule 14A.

- Aadhaar authentication:

- The primary authorised signatory must complete Aadhaar authentication (OTP or biometric).

- At least one promoter or partner must also complete Aadhaar authentication, unless they fall under an exempt category under Section‑25(6D).

- No pending risk or fraud history:

- No cancellation or amendment proceedings should be pending against your existing registration.

- The system should not flag your application as high‑risk based on past compliance or other data checks.

If you meet all these conditions for GST registration under Rule 14a, you can opt for this simplified route when you fill in Form GST REG‑01.

ALSO READ: Income Tax Demand Notice Reply Format

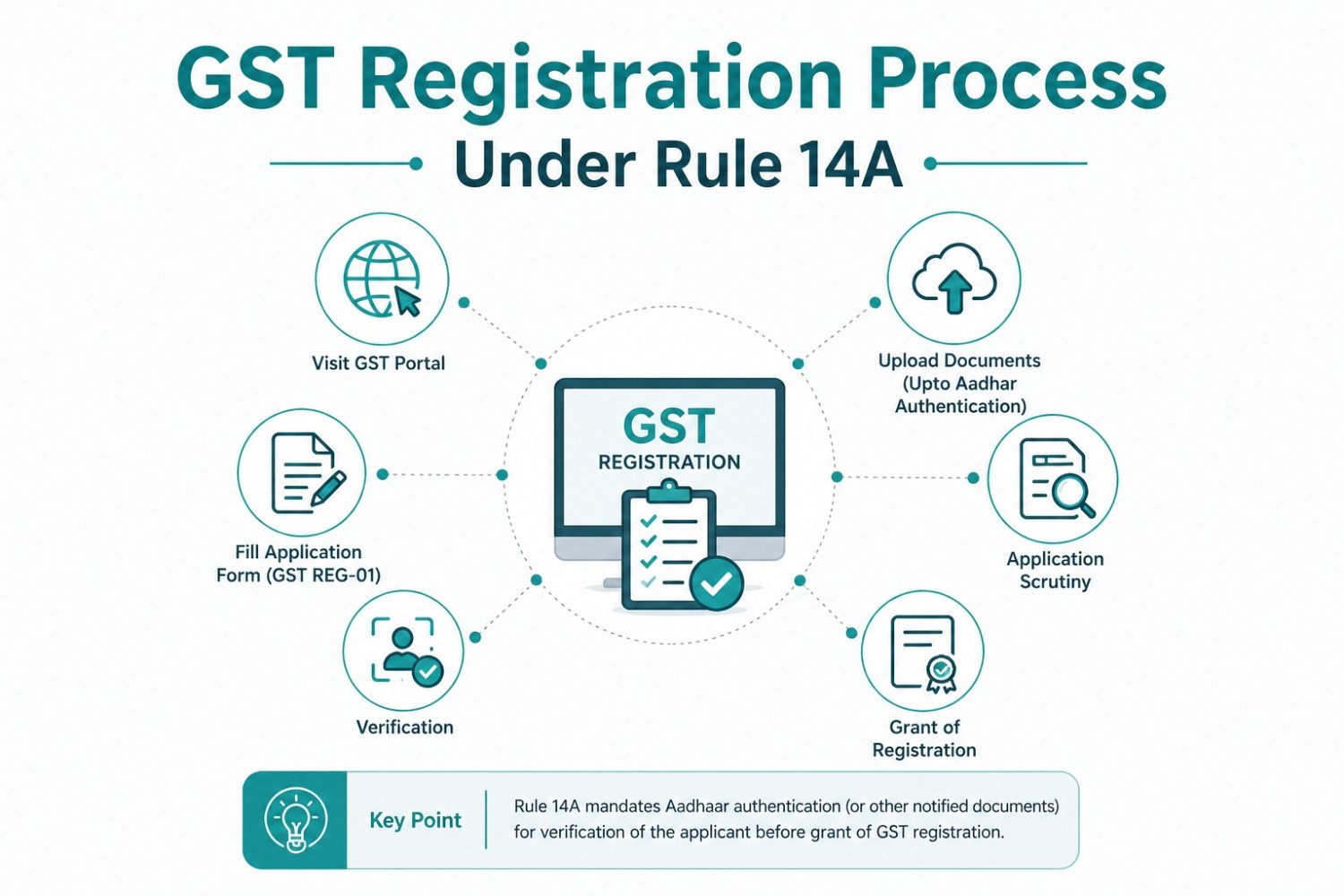

GST Registration Process Under Rule 14A

The gst registration process under rule 14a is almost the same as normal GST registration, except for one important check in the form and the reliance on Aadhaar authentication. Here is a simple step‑by‑step guide:

Step 1: Check eligibility and prepare documents

Before starting, ask:

- Will your monthly output tax on B2B supplies stay under ₹2.5 lakh?

- Do you have valid PAN and Aadhaar details of the authorised signatory and at least one partner?

Common documents you usually need:

- PAN of the business and authorised signatory

- Proof of business constitution (PAN‑based for proprietorship, partnership deed, incorporation certificate, etc.)

- Address proof of the principal place of business

- Mobile number and email for the GST portal

Step 2: Start Form GST REG‑01 on the GST portal

- Go to the GST common portal (https://www.gst.gov.in/).

- Click Services → Registration → New Registration.

- Fill Part A of Form GST REG‑01 (basic details like PAN, mobile, email, State, etc.).

- After submitting Part A, you will get a TRN (Temporary Reference Number).

Step 3: Fill Part B and choose Rule 14A

- Log in using the TRN and open Form GST REG‑01 Part B.

- In the relevant section, select “Yes” for “Option for registration under Rule 14A”.

- Declare that your monthly output tax liability on supplies to registered persons is within the ₹2.5 lakh limit.

At this stage, you are clearly opting for GST registration under Rule 14A instead of the regular route.

Step 4: Complete Aadhaar authentication

- The GST portal will prompt you to complete Aadhaar authentication for the authorised signatory and one partner.

- You can choose OTP or biometric mode.

- If Aadhaar authentication fails or is not completed, you cannot proceed under Rule 14A and must apply through normal registration rules.

Step 5: Submit and wait for electronic approval

- After submitting the form, the system will run automated risk checks based on Aadhaar, PAN, and other data.

- If the system finds your application low‑risk and all conditions are met, your GST registration certificate (Form GST REG‑06) will be issued electronically within three working days.

If risk parameters are triggered, the application may be shifted to the normal verification route (Rule 9/9A), which can take longer and may involve officer queries or document checks.

Benefits and Importance of GST Registration Under Rule 14A

Choosing GST registration under Rule 14A has several advantages for small businesses and professionals.

Key benefits

- Faster approval: You can get GST registration within three working days, compared to the longer normal process that may involve physical verification.

- Less paperwork: No physical verification of business premises is required for eligible applicants.

- Digital‑only workflow: From Aadhaar authentication to certificate generation, the entire gst registration process under rule 14a is online, which suits tech‑savvy startups and freelancers.

- Good for low-B2B businesses: Small traders, service providers, and professionals primarily supplying to registered persons with low monthly tax can use this route.

When it is useful

- New businesses are testing the market.

- Professionals like consultants, freelancers, and small service providers.

- Small traders maintain controlled and predictable B2B tax exposure.

If you are unsure whether you meet the eligibility conditions, firms like KKS Capital Advisor can review your numbers and help you choose the right registration route.

Common Mistakes and How to Avoid Them

Even though the process looks simple, applicants often make mistakes that delay or block registration under Rule 14A.

Typical errors

- Incorrect tax liability estimate:

- Some taxpayers assume the limit is based on turnover, but Rule 14A uses output tax liability.

- If your B2B tax exceeds ₹2.5 lakh in any month, you must exit Rule 14A and apply for normal registration.

- Not completing Aadhaar authentication:

- Skipping or failing Aadhaar checks makes you ineligible for Rule 14A. You then have to restart via normal registration.

- Using multiple PAN‑State combinations under Rule 14A:

- Rule 14A restricts one registration per State/UT under the same PAN. Trying to create another such registration can cause rejection or compliance issues.

- Fake or mismatched details:

- Wrong PAN, address, or business‑activity details can trigger system alerts and shift your application to manual scrutiny.

Best practices

- Double‑check your B2B tax liability for each month and keep a simple record.

- Use Aadhaar only through the GST portal; never share OTPs or biometric details with third parties.

- Get help from a GST consultant (for example, KKS Capital Advisor) if you are new to GST or have complex business structures.

Table: Rule 14A vs Normal GST Registration

| Aspect | GST Registration Under Rule 14A | Normal GST Registration |

| Timeline | Up to 3 working days once Aadhaar is done and there are no risk flags. | No fixed timeline; may take longer due to manual checks. |

| Manual verification | Not required for low‑risk cases. | Possible physical verification or officer queries. |

| Aadhaar authentication | Mandatory for the authorised signatory and one partner. | Optional or not required in some cases. |

| Eligibility | Only for low‑B2B tax liability (<₹2.5 lakh/month). | Open to all taxpayers, including high‑turnover businesses. |

| Use case | Small, low‑risk, digital‑first businesses. | Large businesses, complex operations, or those exceeding Rule 14A conditions. |

Conclusion

GST registration under Rule 14A is a smart choice for small taxpayers who want a quick, digital, and low‑hassle GST registration process. As long as your monthly output tax liability on B2B supplies stays under ₹2.5 lakh and you complete Aadhaar authentication correctly, you can enjoy faster approval and fewer manual checks.

However, the scheme is not automatic or risk‑free. You must monitor your tax liability, keep records clean, and exit Rule 14A in time if your business grows.

If you want to avoid common mistakes and ensure your GST registration under Rule 14a conditions are met, you can consult a professional firm like KKS Capital Advisor to guide you through the application and beyond.

Need help with GST Registration in Gurgaon under Rule 14A or regular GST compliance? Contact KKS Capital Advisor today for expert support tailored to your business size and sector.